BHP Coking Coal Sale: Hate Me Now, Love Me Later For Buying It

BHP Coking Coal Sale: Hate Me Now, Love Me Later For Buying It

With the fiscal year end closing down under this weekend, we come to a very special time, the North American summer. For most this means baseball games, holidays, days at the beach or lake, golf, children at home all day or away at camp if you planned ahead, but for a select few insane people it’s the blackout period into Australian fiscal year reporting season.

So let’s get the first exciting part of this out of the way, because on-market buybacks are so strange/abnormal in Australia due to the fully franked dividend mechanism and the off-market buyback mechanism (the latter no longer being available), there does not yet appear to be a way for coal companies like Whitehaven to put their buybacks on autopilot with a broker even during the quiet period.

So for the next 7 weeks, we will get no daily buyback report. And that makes this marsupial sad in a way. But would note that if Newcastle coal spot price decides to make moves in the next 2 months, that will likely matter more than the lack of buyback activity.

But bringing this up because we have a sort of Sword of Damocles dangling over the coal space – who is going to buy Blackwater and Daunia from BMA/BHP?

We know from priors BHP likes to announce these sorts of things simultaneously with their FY results in late August so, safe to say we have another fun game of speculation to play while no buybacks are happening.

The Australian financial press has reported there are 6 finalists:

· BUMA (Indonesian mining contractor)

· Peabody

· Coronado

· Whitehaven

· Yancoal

· Stanmore (who was NOT a finalist but then brought back into the fold)

For the sake of brevity, not going to get into “who actually needs it more” as it relates to each of the bidders. What’s actually interesting is the eventual transaction structure. Because as we’ve noticed with other various events in the last couple years and quarters, there is really only one western pool of capital that can scrounge up multiple billions to acquire coal assets and, well, safe to presume their hearts and minds are on British Columbia right now.

So BHP has a little bit of a conundrum. They are selling two non-core coal mines but they have multiple agendas which are very difficult to align with our current ESG word:

1) Maximize value

2) High grade the BHP portfolio

3) Put an Australian asset in hands that won’t embarrass BHP

To be clear, my suspicion here is #3 is a much bigger issue than #1. BHP has made the decision to high grade the “non-ESG” portion of its portfolio and whether they get the last $100MM or even $1 billion of value does not really matter if the operator is not dependable (considering the overall number of fixed assets/operations BHP has in Australia besides Blackwater and Daunia).

Alas, BHP does not want to be embarrassed (see Stanmore getting kicked for winning the last one, now being brought back into the fold).

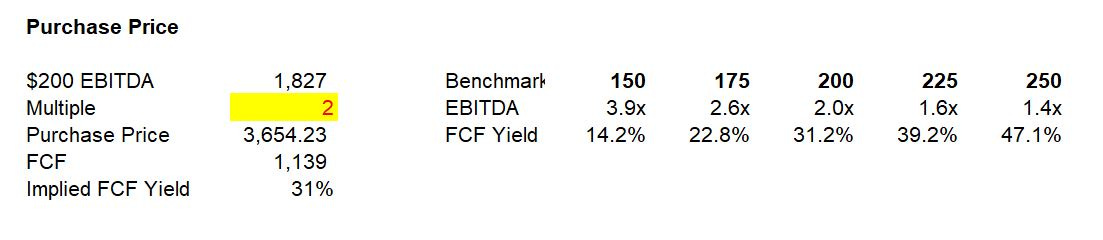

But of these finalists, who has A$3.6 billion to spend (Eucalyptus estimate of 2x EBITDA at $200/t benchmark coking coal) to buy these assets especially if there is no access to bank/credit financing?

The answer is there simply isn’t anyone but Glencore who has the capability, the mandate, or the will to write a check like that up front. And again, Glencore is a little busy right now in Canada chasing down the only coking coal business globally that rivals BMA for scale and quality.

And we haven’t even spoken about how for multiple finalists, their shareholders simply want shareholder returns – dividends and buybacks.

Now to be clear, the eucalyptus tree does not have access to any data room or internal forecasts for Blackwater or Daunia. Based on many conversations with multiple parties over the course of 2023, have been soft guided to a couple key figures on each of these assets.

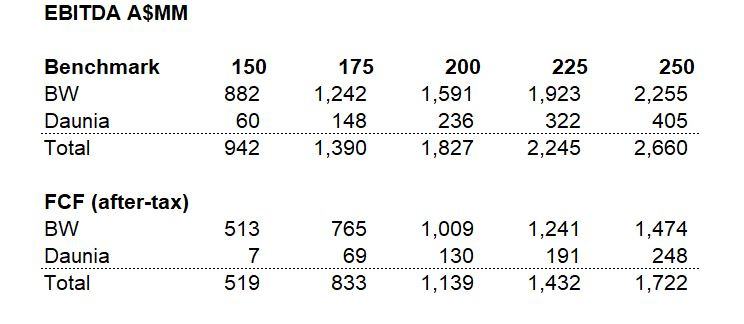

Blackwater: ~12MM tonnes sales volume, 90% benchmark realization, A$1.4Bn cash cost, A$150MM recurring capex

Daunia: ~3.5MM tonnes sales volume, 75% benchmark realization, A$500MM cash cost, A$50MM capex

These numbers may be off the mark but for the sake of this exercise, let’s assume they are the least worst assumptions we can have without an NDA.

And for good measure, the FY22 BHP annual report lists the Blackwater reserve life at 24 years and Daunia at 17 years (so likely more at both considering resource conversion to reserves).

For our purposes here, I think it’s a safe assumption to assume both of these operations will be in production come 2050 if the met coal market is of similar size to its current form.

So that brings us to a key question, what are these assets worth?

We all know (or at least anyone whose listened to my rantings for any period of time) know public market valuations for coal equities are at offensively low multiples. The market is very much pricing for a world where we don’t need coal (met or thermal) by 2030 or 2035 or there is never another profitable period beyond the next couple years. It’s the only way to synchronize the 2023/2024 FCF yields with a “yea this is a reasonable reflective of NAV” conclusion.

So BHP runs into its first conundrum, how in the world do you get your bidding audience to think optimistically about future cycles, optionality, and upside convexity when they have access to that same expression via their own shares on market?

Going to assume it’s one deal and not two distinct deals just for simplicity here but ~15MM tonnes per year coking coal production is up there with Alpha Metallurgical Resources (listed in New York) with a ~US$2.4Bn market cap with all excess cash beyond $300MM minimum liquidity committed to shareholder capital returns. And as we’ve discussed before, the boys and girls in Zug are focused on British Columbia right now.

So two key questions:

1) What to value these assets at?

2) Is there even the ability to pay?

Well first, where I’ve settled out is the right value is ~2x EBITDA using $200/t benchmark met coal.

I think this reflect the reality that the old “$130 trough, $150 mid-cycle, $175 incentive price” talk of 2016-2019 is stale and out the window. I refer you all to a famous slide Teck loved to trot out at their annual investor day that despite the broker consensus for LT coking coal being somewhere between $130 and $150/t, the 2010s averaged $180-190/t. It was extremely volatile around that average but that nonetheless was the average.

That equates to purchase price of ~A$3.6Bn and a FCF yield of 14.2% at $150/t benchmark, 31.2% at $200/t, and 47% at $250/t.

Think that’s a fair spread of scenarios and valuations for a buyer and a seller here.

Alas, A$3.6Bn is ~US$2.4Bn, and that’s a lot of capital for a list of buyers that (ex-Indonesia and Chinese affiliated parties) have no access to credit markets.

And so an idea came boomeranging back through the eucalyptus tree pondering on this as everyone is petrified their coal long will be “the one stupid enough to do it”. It’s time to dust off the underlying Elk Valley Resources financial engineering.

A modest proposal from the koala:

· A$1.0Bn cash up front

· 80% after-tax FCF for the first four years starting June 30th, 2023 goes to BHP/BMA

Having modeled this out at $150-250/t benchmark coking coal prices, and using a 15% discount rate to present value the earn out stream…

You get to a world where BHP/BMA will receive in present value terms the full value of the purchase price, but even more interesting, at the same time, let’s take a look at what 4 year earn out period free cash flow looks like to the acquiror.

We all see that basically at $200/t benchmark coking coal the acquiror receives back their A$1.0Bn up front payment in 4 years. So effectively, for A$1.0Bn and being able to operate these assets according to plan, you have bought almost a “free option” on 15+ million annual tonnes of coking coal production from 2028 onward.

Now shareholders, particularly fast money institutional investors and multi-manager/pod hedge funds who care about P&L tomorrow and only this bonus cycle will freak out. “Koala, there is no buybacks, these companies are the only natural buyers of their stock, everyone who really believes in coal already has invested. This company will be my short in my coal book because no buyback…” To be honest, I can already hear the crescendo.

But actually, if you are invested in a publicly traded coal producer, I don’t care whether its AMR buying back its stock (so getting longer the front of the commodities forward curve) or HCC building Blue Creek (so getting longer the long dated back end of the forward curve) the real win comes from the natural passage of time and the markets either:

A) Realizing Teck was on to something with that resilience of steelmaking coal presentation, and we will be using material amounts of hard coking coal well past 2050

B) You wake up in 3 years and have a full payback on your initial investment in terms of FCF (though in the case of HCC or whomever buys Blackwater and Daunia, some of that will have been re-invested into the business)

But truthfully, if you are invested in coking coal equities today, it’s because you believe in Option A and see this mass delusion coupled with Queensland usurious royalty regime has destroyed any capital investment in the coking coal industry besides Blue Creek, so despite what everyone says, the long term average price of “benchmark” FOB Queensland Low Vol Coking Coal starts with a 2, not a 1 ($200+/tonne to be clear).

Everything I say here is predicated on the acquiror being able to properly operate and deliver on the plan for Blackwater and Daunia. If you cannot operate competently, will then nothing else really matters.

But the more I’ve looked at this with limited information/disclosure around the asset, if structured with some EVR style financial engineering, I think the acquiror of Blackwater and Daunia is likely to get an absolute slam dunk deal.

A chance to spend ~A$1Bn up front to get your hands on 15+ million tonnes per year of quality coking coal unencumbered in four years. And in those four years you basically recover your up front payment if coking coal averages >$200/t.

The internal rate of return (IRR) also looks phenomenal as you think about it at various coking coal prices as well.

The after-tax IRR doesn’t look too shabby either if you believe the ESG dreamers that we won’t need coking coal come some time in the 2030s either. You just have to be ready to have some patience and let the laws of physics, chemistry, economics and reality do their thing.

To no ones surprise, the koala is probably most familiar with Whitehaven Coal, where I am a shareholder. And what inspired this thinking was about a month ago looking at the A$2Bn of unencumbered net cash on the balance sheet as of end of March 2023, I realized, and tweeted, that given all the blackout periods, even if Whitehaven did not generate a single incremental dollar of free cash flow, at A$6/sh and ~9MM shares average daily volume, at 10% daily volume, Whitehaven wouldn’t run out of net cash buying back stock for probably 2 years.

So the Koala leaves you with a simple question – would you be angry as a Whitehaven shareholder if Paul & Kevin spent A$1Bn of said A$2Bn on these coal mines up front, and there was still ~A$1Bn net cash on the balance sheet to keep funding the buybacks and dividends along side ongoing free cash flow generation?

To be frank I think there will be both a relief rally in many of these names for “oh thank god they didn’t buy it” but with the right structure like proposed here I think the transaction could be a positive catalyst for the buyer as well.

You may hate the idea of this now, but you’ll love it later.

And that is the simple joy of being an investor in coal equities in the 2020s whether it’s a bull market or a bear market for the spot price.

And besides, while A$1Bn at A$7.00/share is 143MM shares (~18% total shares outstanding) of Whitehaven Coal, 15MM tonnes (or even just 12MM tonnes from Blackwater) would effectively double the production per share of Whitehaven Coal once the earn out was over while tilting the mix towards met coal (funny, isn’t that a big reason Glencore wants to buy Teck’s coal business). And that is a far more accretive use of capital if you are a coal investor.

So to whichever management team is sitting there wanting to buy Blackwater and Daunia from BHP/BMA, as long as your disciplined about valuation and thoughtful about structuring, the Koala says be brave, do it.

Great write up

Well written!